Links

NEXI steps up support for Japanese shipbuilders

It has been a busy September for Nippon Export and Investment Insurance (“NEXI”), having participated in two ship export transactions. In the first transaction, a group of lenders, comprising Japan Bank for International Cooperation (“JBIC”), Sumitomo Mitsui Banking Corporation and BNP Paribas Tokyo Branch, have agreed to extend loans of JPY 9.4 billion (USD 122.6 million) to Korea’s Hanjin Shipping for the financing of four Kamsarmax bulk carriers. The ships will be built by Tsuneishi Shipbuilding in Japan. In a typical ECA arrangement for Korean shipowners, JBIC and commercial lenders will disburse the loan through Korea Development Bank and NEXI will underwrite the buyer’s credit insurance for the loans provided by the commercial banks.

In the second transaction, NEXI provided a USD 27.5 million buyer’s credit insurance for a loan to a Singaporean subsidiary of Wallenius Lines AB, a major shipping company in Sweden, for purchase of a pure car & truck carrier (“PCTC”) built by Mitsubishi Heavy Industries. The loans are provided by JBIC and the Bank of Tokyo-Mitsubishi UFJ (“BTMU”). PCTCs are designed to carry a spectrum of vehicles including automobiles, trucks, buses, and tall construction/heavy machinery. And just on Wednesday, NEXI participated in a loan provided to Mundra Port & Special Economic Zone limited, Indian subsidiary of Adani Enterprises for the purchase of a tugboat built by Kanagawa Dockyard. JBIC and BTMU were the participating lenders. Continue Reading

Pacific Shipping Trust Seeks Delisting

The Singapore shipping trust sector suffered a major setback this week after forerunner Pacific Shipping Trust (“PST”) announced intentions to voluntarily delist from the Singapore Exchange. PST was listed way back in May 2006 amid fanfare and was touted as a new attractive asset class in the form of a “maritime annuity” for investors. But after years of lacklustre share performance and lukewarm investor appetite, its parent company Pacific International Lines (“PIL”) has decided it is time to call it a day.

PIL cited the need for greater operating flexibility as one of the reasons for PST’s delisting. PST’s growth potential has been hampered by the need to benchmark any potential acquisition against its distribution yield and making sure that any acquisitions are accretive to unitholders. This is difficult to accomplish in reality because the distribution yield is a function of the prevailing trading prices of the units and the lacklustre share performance over the years has made it challenging for the shipping trust to source for yield accretive transactions. At the same time, the amount of debt that PST can take on for each acquisition is limited by and subject to credit, debt service and prudence considerations. The delisting will also eliminate the costs of compliance with the listing rules and regulations, allowing PST to focus its resources on its business operations. “PST as a non-listed entity will have greater operational flexibility to pursue opportunities and make investment decisions without being constrained by market-based yield expectations, market sentiment and price volatility,” PIL said. Continue Reading

Swiber Seeks Shareholders’ Mandate for Preference Shares Issue

Perpetual securities are uncommon in Asia, but this has not deterred a number of offshore services companies in Singapore from looking into tapping this source of liquidity. Singapore listed offshore services firm Swiber Holdings is seeking shareholders’ approval to allot and issue convertible preference shares, which if converted in full into conversion shares at the conversion price, will not result in the issuance of not more than 40% of the enlarged share capital of the company.

Preference shares belong to a hybrid investment class, which is senior to common shares but are subordinate to bonds. Analysts generally perceive preference shares as a loan to the company, because preference shareholders are not entitled to normal voting rights but are entitled to dividends. In Swiber’s proposed issue, the company is offering convertible preference shares that provide investors the option to exchange for a predetermined number of the company’s common stock. A convertible preference share has features similar to a convertible bond. The differences lie in that preference shares are subordinated to debt of the issuing company and are usually perpetual securities with no maturity date.

Dividends to Swiber’s preference shareholders are cumulative and payable semi-annually at a fixed rate per annum, and there is a built-in dividend step up which may be activated upon events such as the deference of dividends. The issuer may, at its sole discretion, choose to defer dividend payment to the next dividend date. However, during this period, the dividend stopper will kick in and the issuer will not be allowed to declare or pay any dividends, or repurchase or redeem shares ranking junior to the preference shares.

Preference shares are and are not redeemable at the option of the preference shareholders. The issuer has the right but not the obligation to redeem the preference shares on any stipulated optional redemption date, occurrence of a tax event (any change in any tax law or regulation in Singapore) or occurrence of an accounting event (any change in the accounting standards applicable to the company). For the benefit of preference shareholders, preference shares are convertible into fully paid conversion shares during the conversion period. This means that there could be an increase in the number of shares outstanding in the future, and may be earnings dilutive to the existing shareholders. We expect more details to be announced at a later date.

Swiber intends to distribute the preference shares to institutional and accredited investors on a private placement basis and proceeds will be used for general working capital and capital expenditure.

Business as Usual for Now

Shipowners in Asia are bracing for the potential negative repercussions from the worsening banking crisis in Europe. After all, it was not too long ago when the lack of trade finance caused the BDI to plunge to a low of 663 points on 5 December 2008. Thankfully, a quick check with a number of commodity traders has suggested that the situation is still healthy on the ground. Trade finance is still available and cargoes are moving.

Even so, there are increasing worries that the major European shipping banks might no longer be able to continue provide funding to the shipping industry. Financial institutions in Asia and elsewhere have been reducing credit lines and exposures to European banks in the recent months and this have forced many European lenders to swap lines offered by the European Central Bank for US dollars. Bank of China for example is said to have stopped the counterparty dealings with several European banks. And if more banks are to follow suit, European banks will find it even more difficult to raise US dollars due to concerns over counterparty credit risks. Anxiety about the European debt crisis is driving up sharp spikes in the credit default swap spreads on major shipping banks, suggesting that the markets are increasingly cautious about the credit prospects of these lenders. Continue Reading

Bonds Frenzy Continues in Korea

Historically low interest rates have encouraged investors to chase after high yielding assets and many shipping companies have taken advantage of this low interest environment and strong investor demand for yield to lock in cheaper cost of funds, either to refinance existing debt or build up cash positions. This is especially pronounced in China, Japan and South Korea.

In Korea, the domestic bond market continues to serve as a major source of liquidity for shipping companies. The country’s four largest shipping companies – STX Pan Ocean, Hanjin Shipping, Hyundai Merchant Marine and SK Shipping have collectively raised USD 1.56 billion since the beginning of this year, and this amount could well exceed the total bond issues raised in 2010. Continue Reading

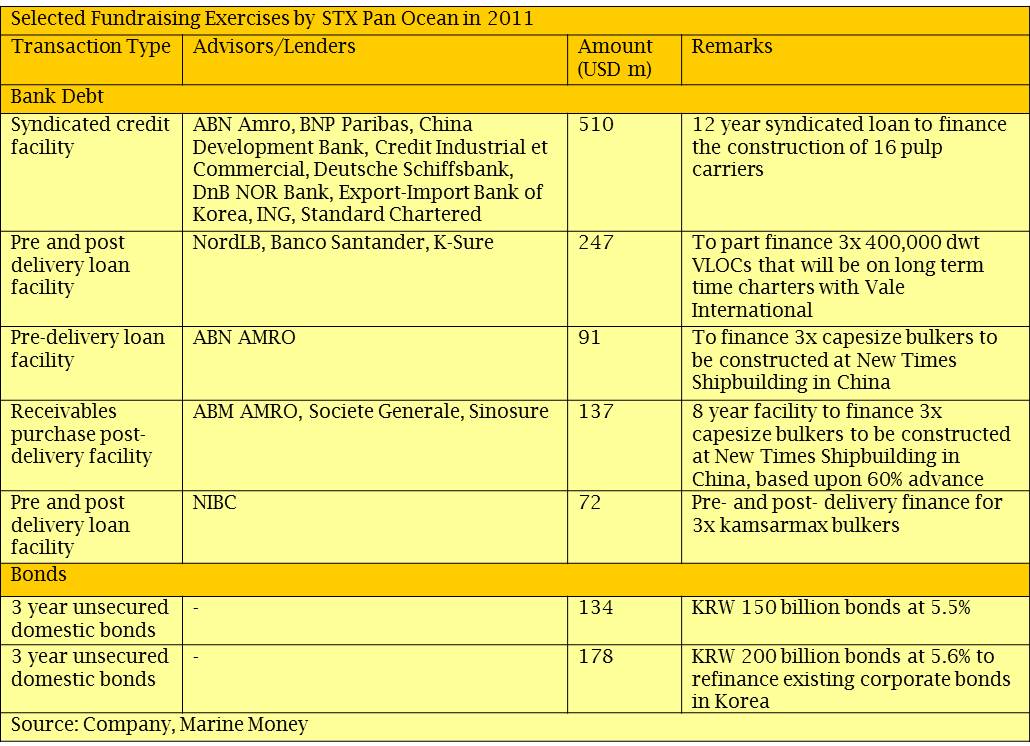

STX Pan Ocean Closes USD 510 million Syndication

South Korea’s STX Pan Ocean has secured a USD 510 million 12 year syndicated loan facility with a consortium of nine domestic and international lenders, comprising ABN AMRO, BNP Paribas, China Development Bank, Credit Industrial et Commercial, Deutsche Schiffsbank, DnB NOR Bank, Export-Import Bank of Korea, ING and Standard Chartered.

In October 2010, the company broke new ground and entered into the global pulp transportation market by securing the large consecutive voyage contract with the world’s largest pulp and paper company, Brazil’s Fibria Celulose. To fulfil this 25 year USD 5 billion contract that commences from 2012, STX Pan Ocean ordered 20 pulp carriers from another STX Group company, STX Offshore & Shipbuilding. Proceeds from the latest loan will be used to cover 70% of the total cost in the construction of 16 pulp carriers. Funding for the remaining

four vessels will be secured at a later date.

STX Pan Ocean has been actively raising funds since the start of this year to finance capex requirements through a combination of shipping banks, export credit agencies and domestic corporate bonds. We provide a list of recent transactions in the accompanying table.

CNMIEC Offers Preferential Loan to Bangladesh Shipping Corporation

CNMIEC Offers Preferential Loan to Bangladesh Shipping Corporation

Chinese state-owned trading house, China National Machinery Import & Export Corporation (“CNMIEC”), has approached Bangladesh Shipping Corporation (“BSC”) for the sale of 7 vessels worth at least USD 251 million. According to local press, CNMIEC seeks to sell two product tankers of up to 35,000 dwt at USD 43.5 million apiece, two bulk carriers of up to 38,000 dwt at USD 31 million apiece, two small container ships between 1,100 – 1,200 TEUs at USD 20 million each and an oil tanker at a price tag of USD 62 million to the Bangladeshi national carrier.

CNMIEC will be throwing in a deal sweetener in the form of a preferential loan. The trading house is confident that it will be able to secure a preferential loan of 12-13 years for BSC with a grace period of 2-3 years, at an interest rate between 2.5 – 3.0%. The proposal has been submitted to the government for review.

Bangladesh has been planning to build up its national fleet to reduce reliance on hiring foreign vessels for its imports.

CIMC Raffles and China Merchants Energy Shipping Eye More Equity

The volatility in the stock markets has not dampened the spirits of Chinese shipbuilder CIMC Raffles and major Chinese international oil tanker operator China Merchants Energy Shipping to tap more equity.

CIMC Raffles is proposing to undertake a non-renounceable non-underwritten one for two rights issue to raise gross proceeds of approximately USD 102.6 million. The rights shares will be offered at USD 0.50 a piece, which is 46.2% discount to the company’s net asset value per share of USD 0.93 as at 31 December 2010. Proceeds will be used to repay bank borrowings and lower its gearing ratio, improve facilities at its existing shipyards, and fund working capital requirements. Continue Reading

China Rongsheng Inks Another Massive Credit Facility

On Monday, Hong Kong listed China Rongsheng Heavy Industries Group Holdings signed a strategic collaboration agreement worth RMB 30 billion (USD 4.7 billion) with China Development Bank in the Chinese city of Nanjing. A large chunk of the facility will go towards its offshore engineering division. We note that Rongsheng has signed many similar corporative agreements with numerous Chinese lenders including China Exim, Bank of China, China Everbright Bank, China CITIC Bank and Agricultural Bank of China since August 2010, of at least total of over RMB 129.5 billion (USD 20.2 billion!).

We also have more details on Rongsheng’s recently completed USD 220 million offshore syndicated loan. Sole book runner Credit Agricole took up the biggest slice in the loan of USD 40 million while four lead arrangers Societe Generale, Aozora Asia Pacific Finance, Bank of East Asia and Bank of Tokyo-Mitsubishi UFJ committed USD 30 million each. Cathay United Bank chipped in USD 20 million. Italian bank Banca Monte Dei Paschi di Siena, Taiwanese lenders Chang Hwa Commercial Bank and Hua Nan Commercial Bank, as well as Metropolitan Bank and Trust in Philippines rounded up the syndication and contributed USD 10 million each. The loan offers the lenders a margin of LIBOR plus 130 basis points and is guaranteed by China Exim Bank.

Standard Chartered Shows Strong Momentum in Leasing

It was barely a year ago when Standard Chartered Bank introduced its ship leasing services, but all signs are already pointing to the continued popularity of this form of financing. Headed by industry veteran Sander Scheepens, the ship leasing team has been busy since its inception in October 2010, having closed seven transactions of over USD 700 million. Today, the bank’s ship leasing portfolio is made up of 21 ships, across various asset classes including dry bulk carriers, tankers and offshore supply and service vessels. Of the total leased fleet, 15 vessels are currently under-construction and 6 in the water. The ships are contracted on operating leases of between 7 to 12 years, mostly with existing clients of the bank who are based in Asia.

According to Mr. Scheepens, the sentiments have since changed and there is a “feeling of crisis” in the current market. “A year ago, people were careful but the panic was over. Container shipping companies were posting record profits and there was moderate confidence in the dry bulk sector. Today, markets are under a lot of pressure again. Therefore companies are starting to look at other financing options, given that bank debt may be less available than before. We are getting more leads, but that doesn’t mean it is easier to do transactions,” he said. Continue Reading

The Official Guide To Marine Finance Providers

Shipping Index