Links

Market Commentary – 01/25/2007

When does A, B, C become X, Y, Z? When the IMO changes the rules.

They’ve been discussed at the IMO in its various committees for years, and now they’ve come into force.

Stricter rules on carrying vegetable oils in bulk by ship are among the changes introduced by amendments to the International Convention for the Prevention of Pollution from Ships, 1973, as modified by the Protocol of 1978 relating thereto (MARPOL 73/78), which entered into force on 1 January 2007.

The revised Annex II regulations on carriage of noxious liquid substances carried in bulk (including chemicals and vegetable oils) introduce significant changes to the way certain products may be transported, in order to protect the marine environment from harm. Continue Reading

Open-Ended Funds – 01/25/2007

“Open Waters” Open-Ended

Combining worldwide shipping and banking expertise, Lloyd Fonds AG together with Oppenheim Pramerica formed the first open-ended shipping fund in the world called LF Open Waters OP (“Open Waters”) at the end of last year. Resident in Luxemburg, Open Waters takes the form of a Société d’Investissement à Capital Variable (“SICAV”), a structure which makes the fund open-ended and allows the return of shares to the fund to allow investors to realize their gains. With a SICAV, the purchase and redemption of shares leads to a “breathing” equity or a “constant IPO” structure, which means that the equity accounts will increase or decrease depending on the net trading activity. In short, the fund is fully flexible and designed for day-to-day trading. To accommodate the structure and to service any major share redemptions, the fund will keep a liquidity reserve of 20% relating to its equity, either by means of liquid assets or an unclaimed debt facility. Continue Reading

The Week in Review – 01/25/2007

The year is off to a brisk start, with the Norwegian bond market booming, particularly in sectors related to energy. And the optimism spreads across the Atlantic, with Stena and ACL both tendering for outstanding issues for in favor of cheaper and less restrictive debt. Meanwhile Bergesen Worldwide gives the first indications that it might be more than a passive investor in General Maritime while Genco hints at aspirations to the role of dry bulk consolidator with the filing of a shelf registration to raise up to $500 million in capital. Xylas Group of Greece continues the growing stream of cement sector financings we have been witnessing over the past few months, while Lloyd Fonds has formed the first open-ended shipping fund in the world. Finally this week we take a look at what the new 2007 IMO regulations really mean and visit the conflict of interest that haunts those shipowners with both public and private fleets.

And of course, there are forums! Continue Reading

The Week in Review – 01/18/2007

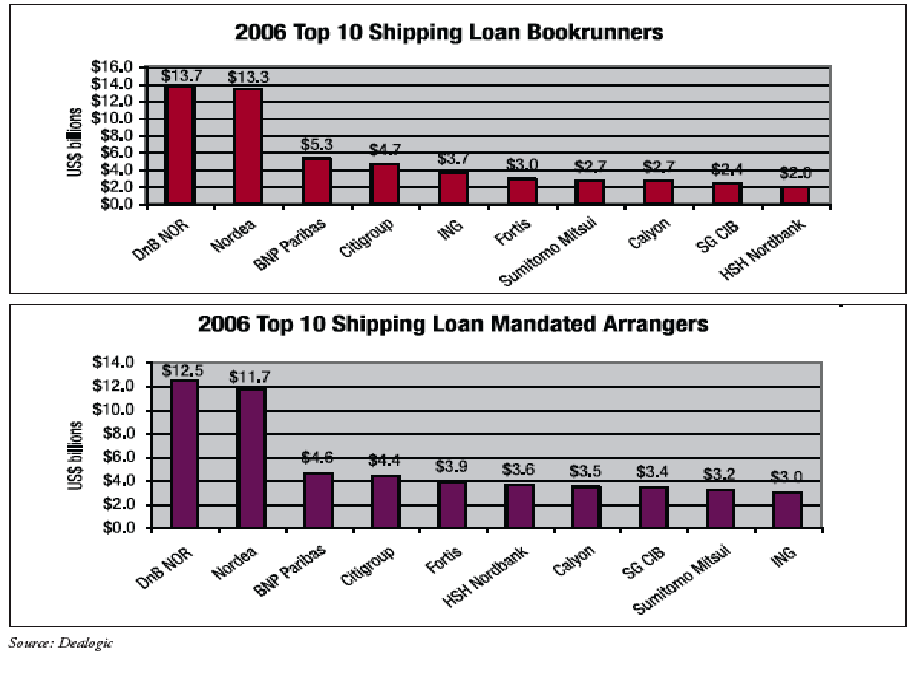

A Record $76 Billion Year for the Syndicated Loan Market

Two weeks into 2007, and the results are in. According to the data Dealogic has compiled, last year was once again a record year for the shipping loan market, with syndicated debt providing $76 billion in capital to the industry as compared to $66 billion in 2005. Long a source of controversy, the results shown include syndicated loans that were secured by anything that floats, including floating rigs, cruise ships and tugs, as well as unsecured deals whose borrowers’ primary industry is shipping.

Not surprisingly, Scandinavian banks DnB NOR and Nordea have once again topped the list, with both banks winning over $13 billion in bookrunning credit, while DnB NOR had $12.5 billion in mandated arranger credit versus Nordea’s $11.7 billion. BNP Paribas has made a significant leap up to third on both lists, with over $5.3 billion in bookrunning credit and $4.6 billion in mandated arranger credit. BNP is followed closely by Citigroup, with ING, Fortis, and HSH Nordbank also putting in strong performances.

As we have said in the past, it is important not to lose sight of the real winners here: the shipowners who hardworking banks are able to provide an ever-growing pool of available capital through syndicated debt issuance. Congratulations to all!!

Norway: A January Hotspot

League tables aside, we are constantly struck by the amount of liquidity that exists in Oslo for maritime ventures of all kinds. This week was no exception; despite oil prices that fell briefly below $50 a barrel, the spotlight was on the offshore market with BW Offshore raising equity to invest in Prosafe and Fredriksen’s creation of new, publicly listed heavy-lift company Sealift.

BW

Offshore Issues New Shares, Ups Prosafe Stake

Bergesen Worldwide Offshore this week completed a placement managed by Carnegie of 43,605,016 new shares at a subscription price of NOK 26.0 per share. The equity issue raised approximately NOK 1.1 billion, or $170 million. The largest publicly held US mutual fund company, Franklin Resources, purchasedf 8,397,100 shares in BW Offshore, bringing its holding up to 11.5%, valued at around $95 million.

The placement was done to fund BW Offshore’s purchase of 12,257,085 shares in Prosafe at NOK 86.0 per share for about $163 million. This brings the number of Prosafe shares under the control of BW interests up to 51,932,990, a 22.6% stake in the company worth around $690 million. You may remember Prosafe from its attempted acquisition of Petrojarl, but now the tables are turned. BW Offshore has indicated that it is interested in being an active participant in consolidation in the FPSO industry and that it believes “a transaction” with Prosafe would be a good fit. There is no question that consolidation is coming in the offshore industry, but there is certainly some suspense as to who the consolidators will be.

Shifting Assets

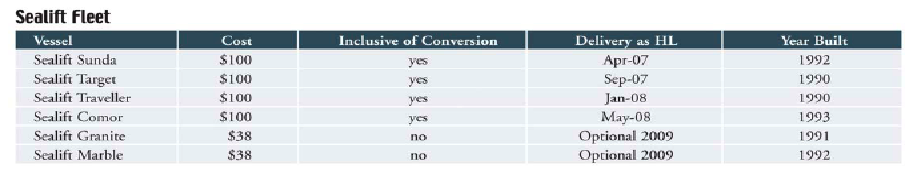

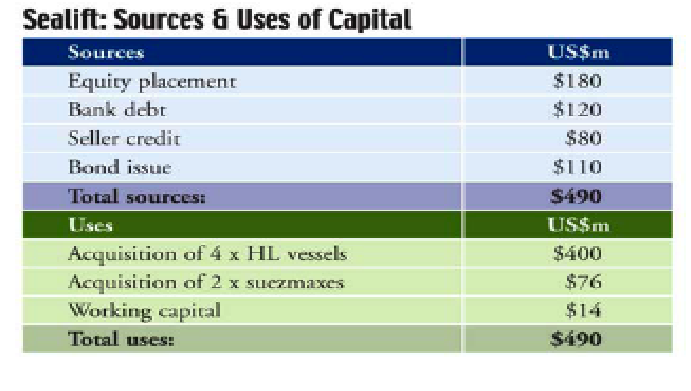

It’s been a busy week within the confines of Fredriksen’s mighty maritime empire, as the magnate and his management adeptly shift around assets, ensuring investors in each entity exposure to the promised niche while developing prospects in the heavylift sector. Ship Finance has purchased a $210 million rig from Seadrill and leased it back for 15 years while at the same time selling five single skin suezmax tankers to Frontline. Frontline has made arrangement for the conversion of these tankers along with one other to heavy-lift vessels for the creation of new public company Sealift. Sealift has with the help of Pareto, Carnegie, Fearnley Fonds and Nordea, as well as Frontline, raised $490 million to purchase the future heavy-lift vessels.

Ship Finance in $210 million Sale Leaseback with Seadrill

Starting with the simpler of the transactions, Ship Finance International (SFL), initially created as a publicly listed lessor for Frontline, has continued to diversify its asset base – though not its exposure to its ultimate counterparty – with the acquisition and commensurate 15-year lease back of jack-up rig West Prospero from Fredriksen oil services firm Seadrill. SFL paid $210 million for the rig. The aggregate lease payments for the first three years total $120 million, after which Seadrill has a $142 million purchase option. The aggregate lease payment over the 15-year period is $306 million, at the end of which Seadrill has a $60 million purchase option.

SFL and Seadrill executed a similar deal together in July of 2006, with the $210 million sale and 15-year lease back of another jack-up rig. Seadrill COO and CFO Alf Thorkildsen has described the two transactions as a way to free up capital and boost scope for financial leverage. The company is currently focusing on a building program consisting of 10 rigs and two deepwater drillships.

SFL Sells to Frontline, Pays Penalty

Shortly after this transaction was announced, SFL brought its liquidity back up over $1 billion with the sale to Frontline of five single hull suezmax tankers for a gross price of $183.7 million, or approximately $36.7 million apiece. However, due to the fact that the sale of these vessels by SFL to Frontline meant the early termination of SFL’s charters to Frontline, SFL had to pay $62 million in compensation to Frontline along with the sale, reducing the effective price paid to $121.7 million. After accounting for $14.2 million in debt on the vessels, SFL netted around $107 million in cash. Importantly, the transaction brings SFL’s single hull fleet down to 11 vessels three years in advance of the 2010 single hull phase-out deadline.

A New Lease on Life

Three years away from being obsolete, the single skin vessels are not assets Fredriksen plans to hold onto, but rather to use as a platform for entering the heavy-lift sector with the new company Sealift.

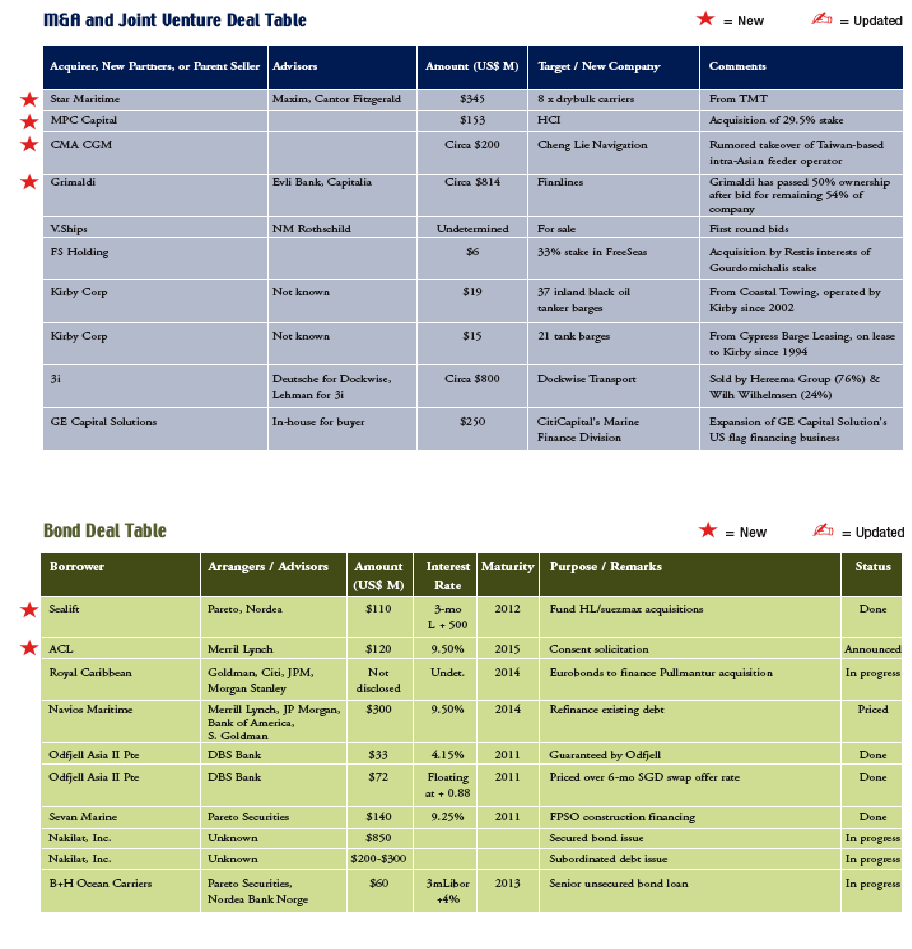

The heavy-lift sector just recently got some unusual attention when the largest player, Dockwise Transportation, was sold by Heerema and Wilh Wilhelmsen to private investment fund 3i for around $800 million all-in under the advisory of Deutsche Bank and Lehman. Dockwise is the dominant player in the heavy-lift segment by a long-shot, controlling a total of eight high end vessels. Cosco has two such vessels and Awilco one, while Fairmount Heavy Transport has two high-end vessels on order. That, in essence, summarizes the world’s high end heavy-lift fleet.

What’s more, Sealift points out that the vast majority of Dockwise’s fleet is over 20 years old and will require replacement. Particularly sensitive to economies of scale, the sector is arguably ripe for consolidation. Sealift’s six potential vessels are set to represent approximately 40% of the global high-end heavy-lift fleet in 2008. In a sector where experienced management and strong customer relationships are particularly essential to success, Sealift has also hired away Dockwise’s CEO Bert Bekker as its own CEO.

Sealift’s focus is the transportation of drilling rigs and offshore modules. High rig rates and strong field development economics have made the industry more attractive as costs for alternative transportation, such as tugs, have increased. Heavy-lift transportation is both faster and safer than alternatives, reducing opportunity costs and insurance costs. At present, transportation by heavy-lift is approximately 50% cheaper than by tug, and current day rates are in the realm of $70,000- $100,000.

One suezmax is currently under conversion at Cosco shipyard in China and is scheduled for delivery in April 2007. The next three vessels are expected to undergo conversion and be operable by May of 2008. The final two, which were sold as suezmax tankers with a conversion option, would not be ready until closer to 2009 if the option is exercised. These two vessels are on commercial and technical management arrangements with Frontline, and Sealift will put out all vessels on bareboat charters to Frontline as long as they are operational as traditional tankers.

Fleet information can be seen more clearly in the table that accompanies this article. Based on the information available, the conversions are expected to take around 7 months and cost in the realm of $40 million. Importantly, Frontline has agreed to bear the risk associated with conversion for the four vessels that have been sold as heavy-lift.

Bank Debt & Sellers Credit

Frontline will fund $80 million of Sealift’s initial debt requirements with a seller credit equal to the conversion cost of the Traveller and Comor to be repaid when the conversion of those two vessels is completed. Sealift is also taking out $120 million in bank debt, or $20 million per suezmax, to be increased to $40 million per heavylift vessel post conversion. Names of lenders were not specified.

Pareto, Carnegie, Fearnley in $180 million Equity Issu

To fund the equity portion of the acquisition, Pareto Securities, Carnegie and Fearnley Fonds managed an offering of 90 million new shares at a subscription price of $2.00 per share, raising a total of $180 million. Frontline has subscribed for at least 1/3 of the equity issue, a $60 million commitment. The subscription period ended on Tuesday January 16.

Shares were to be immediately listed on the OTC and are to be listed on a “well recognized public market” within 12 months. The offering was directed towards a selected group of professional Norwegian and international investors including American qualified institutional buyers

Pareto, Nordea in $110 million Bond Issue at 500 Over

In conjunction with the equity issue, Sealift issued $110 million in second priority mortgage notes at par due 2012. Pareto Securities and Nordea Bank acted as joint lead managers on the issue, which priced at 3- month LIBOR + 500 basis points. Sealift has options to call the bond at 1 year at 104% of par, 2 years at 103%, 3 years at 102% and 4 years at 101%. Associated covenants prohibit Sealift from making any dividend payments, share repurchases or other distributions to shareholders for the first two years after the settlement date, expected in February.

The dividend prohibition makes more sense in light of the fact that Sealift’s heavy-lift fleet will gradually be coming into operation through 2007 and 2008, with further conversions possible in 2009.

Valuation

Based on forecast EBITDA of around $141 million in 2009 and 2010, Sealift company is valued at around 2.6x EV/EBITDA and at about 2.0x P/E. It is hard to say how meaningful these numbers are, however, as in reality Frontline is making a serious bet on the success of the heavy-lift market with the launch of Sealift, and investors are asked to join and share this risk. The majority of the fleet is not yet operational in the sector for which it has been sold, and investors will have to wait at least two years for the fleet to become fully operational and for the company to be able to engage in dividend payments, share buybacks, or other activities that could lead to significant appreciations in share value. At the same time, Fredriksen has once again masterfully shifted around his assets to add a new sector to his portfolio without missing a beat as far as public investment.

A Rising Star

Nearly 13 months after raising $189 million with a blank check IPO in New York, Star Maritime has announced its acquisition target: eight dry bulk carriers owned by Taiwan-based TMT Co., Limited for an aggregate acquisition price of $345.2 million. $120.7 million of this will be payable in shares of common stock of newlyformed Star subsidiary Star Bulk. The remaining $224.5 million is to be funded with a combination of cash in Star’s trust fund and bank debt. The relatively small difference between cash purchase price and the $189 million raised should leave Star a fair amount of wiggle room for finding debt on agreeable terms, but a credit facility is yet to be negotiated.

TMT will also be eligible to earn up to 1,606,962 additional shares if certain revenue hurdles are achieved; TMT and affiliates are expected to own approximately 30% of Star Bulk’s outstanding common shares.

The fleet of vessels to be acquired comprises two capesize, one panamax and five supramax dry bulk carriers with an average age of 10 years. TMT CEO Nobu Su is to serve along with Star sponsor Petros Pappas as non-executive co-chairmen of Star Bulk. Star sponsor Akis Tsirigakis is to serve as Star Bulk’s president and CEO, while George Syllantavos will act as CFO. In a press release, Mr. Tsirigakis called the transaction a combination “of the rich traditions of Asian and Greek shipping”, and indirectly alluded to the transaction as one that could put Star Bulk in the position to be a consolidator in the fragmented dry bulk market.

We look forward to providing more information when Star Maritime files its proxy statement in preparation for a shareholder vote on the proposed merger.

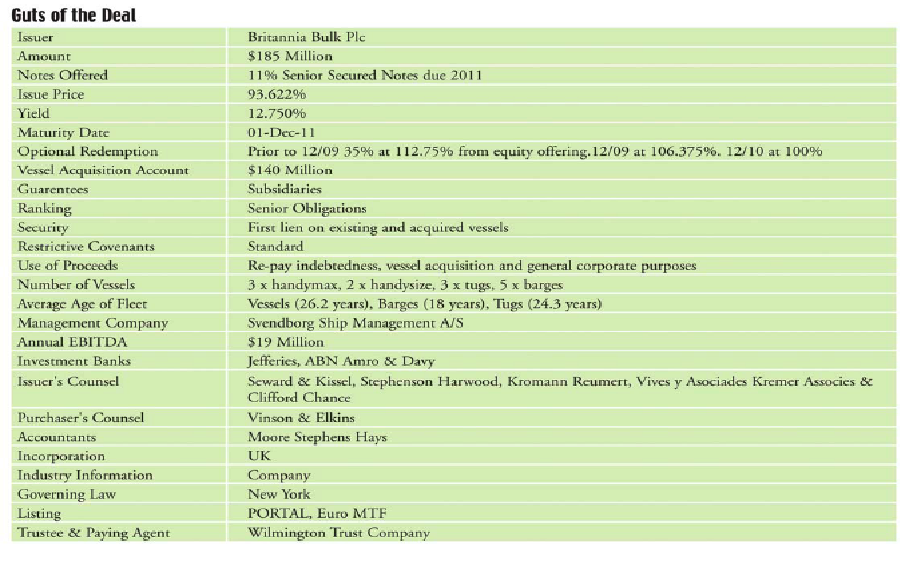

Britannia Bulk Revisited

A couple of months ago, we covered in some detail the successful execution by Jefferies and ABN Amro of the sale of high yield bonds for Britannia. We thought that with the recent acquisition of its first vessel we would take the opportunity to go back and fill in some of the background of the deal, which, in fact, received nominations for the public debt deal of the year award.

Britannia is a niche player in the larger international dry bulk business. It focuses on transporting coal exports from the Baltic region primarily to northern and western Europe. Based upon geography, this trade is characterized by short-hauls and icy conditions and requires knowledgeable management. Trade in this region has grown in recent years based upon increased exports of coal from Russia to Europe. Also unlike most businesses in this segment, the company generates a substantial portion of its income from fixed price COAs, which have terms of up to two years. Key customers include Glencore International AG, Siberian Coal Energy Company and Wegloloks S.A.

As we mentioned previously, the challenge for the bankers was to raise capital to enable this company, which was burdened with a short operating history, high leverage and an old fleet, to modernize and grow. The most suitable product was a high yield bond offering. Despite having to downsize the offer and increase pricing, Jefferies and ABN Amro were successful in raising $185 million in capital, without equity dilution, which was used to pay off existing debt and create a Vessel Acquisition Account of $140 million.

Also in a very interesting structural detail, the company negotiated the ability to prepay up to 35% of the bonds within the first three years from the proceeds of an equity offering at a price of 112.75% plus interest. For the subsequent years, the premium is 106.375% until the last year when the bonds are redeemable at par.

The first use of proceeds occurred in December when Britannia purchased the M/V Atlantica from Peter Dohle for $37 million. The vessel is a 73,538 DWT Panamax bulk carrier built in 1995 at Hyundai Heavy Ulsan.

For further information, we have included the “Guts of the Deal.” We look forward to hearing more from this small niche player with a strong market presence.

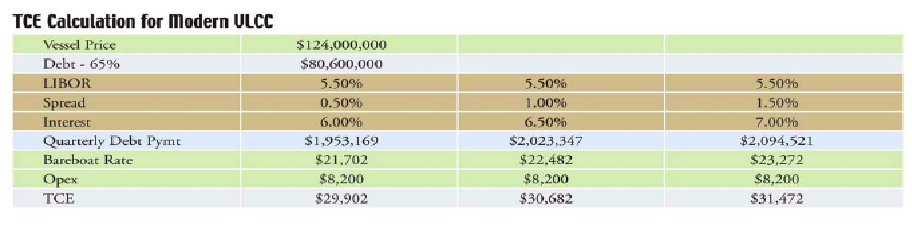

A Mathematical Exercise

With the recent weakness in the tanker markets, and the analysts in general predicting a difficult market in 2007, we thought it might be useful to calculate hypothetical breakeven rates on VLCC tonnage bought in 2006. In truth, these numbers are not truly meaningful in that no banker in his right mind will finance one of these vessels on a project basis unless, of course, it is accompanied by a long-term charter. Instead they are typically financed based upon the borrower’s credit where risk is mitigated by a diversified fleet, cash built up in the good years and existing liquidity lines. Nevertheless, a comparison of the breakeven rates with current market spot rates is indicative of the potential for “bleeding” or egregious profits on a stand-alone asset basis.

For purposes of this exercise, we have made the following assumptions. Data provided by a broker friend on selected VLCC transactions during 2006 indicates an average age and purchase price of 4.3 years and $124 million respectively. Interestingly, data provided by the same broker shows an average newbuilding price, based again upon selected orders, of $122 million with delivery in 2009-2010. For operating expenses, we have assumed $8,200 based upon the latest data in Moore Stephens’ OpCost 2006. For our debt assumptions, we have utilized a LIBOR rate of 5.5% based upon the swap curve for 10-30 years and chose spreads of 50 to 150 basis points to reflect the risk margin. Leverage is conservatively assumed to be 65%. To avoid arguments with respect to the proper term and respective appropriate balloon, we have decided to run the deal for 15 years to a scrap balloon. As we will have only utilized 20 years of an expected life of 25 to 30 years, we have chosen to be use a balloon based upon 45,000 l.d.t. and a historic scrap price of $200. Debt payments are quarterly in arrears. Although our assumptions are easily questioned, we believe the results, shown in the table that accompanies this article, are reasonably representative.

A TCE of approximately $30,000 per day shows there is still margin to protect the downside versus the consensus 2007 VLCC rates of about $43,000 suggested by Messrs. Chappell and Dür discussed last week, with Mr. Kartsonas’ projection of $32,000 being a wild card but certainly more worrisome. On the other hand, the number is also indicative of the magnitude of operating leverage and the consequent excess cash flow generated during strong markets. It was also interesting to note that spread differentials, which purport to reflect risk, are not that meaningful in nominal terms particularly given the size of the debt involved in this instance. .

We would be happy to hear from readers who have better suggestions with respect to our assumptions. In the meanwhile, here is a number for you to keep your eyes on.

Tanker Analytics – 01/11/2007

Same Market Different Views

The wonderful thing about being human is that each person can look at the same facts and come away with a different view or perspective of what the information means. We will leave the theorists to determine whether the influences are chemical, biological or environmental and just enjoy the results of these analyst’s views of the oil market.

On Wednesday, Jonathan Chappell of J.P. Morgan Securities Inc. reiterated his 2007 outlook for the tanker market suggesting that tanker spot markets will continue their decline in 2007. His argument is supply side focused where the “…massive capacity additions (the highest since 1976) and limited scrapping [will] more than [offset] modest demand growth.” Bearing in mind that the supply side is always easier to quantify, Mr. Chappell applies a multiplier to the IEA’s forecast of oil demand growth of 1.7% or 1.43 mbd to calculate a need for 12.9 mdwt of new tanker capacity versus a net fleet increase of 25.6 mdwt (34.1mdwt delivered less 8.5 mdwt removed). Despite the significant supply overhang as well substantial deliveries in the next two years, he sees a measured decline in 2007 of 18-32% in crude tankers and 9-12% in the products tankers. On the other hand, support for rates comes from demand growth, which remains above the 20-year average of 1%, and J.P Morgan’s economic forecast of a relatively solid global economy alleviating concerns about a recession. Other support comes from changing trade patterns with a concomitant increase in the ton-mile multiplier, together with phase-outs, discrimination against single hulls and scrapping. Continue Reading

Market Opportunities – 01/11/2007

Excess Liquidity + High Transaction Costs – Individual Investors = Institutional Investment

In an innovative structure, HSH Nordbank, HSH Gudme Corporate Finance and König & Cie. together created and sold publicly Marenave Schiffahrts AG, the first listed ship-investment company in Germany. This new shipping product was designed to provide institutional investors with an option for long-term investment in the shipping market as an end as well as a tool for diversification of their portfolios. Also by marketing to institutions, the infamous front-end sales costs, associated with the retail market, were brought down to a very competitive level making future projects more viable. The company successfully raised EUR 150.05 million through a sale of shares to such institutions as insurance companies and pension funds. The targeting of institutional financial investors is a current worldwide theme which we have seen in the acquisition of Heidmar, the US assets of P&O, OOIL’s terminals and Teekay Offshore to name a few. Clearly, they have money to put to work, seem less price sensitive than industry participants and have the financial know-how to minimize risk particularly with public vehicles. Continue Reading

The Importance of Management – 01/11/2007

Eyes on V.Ships

A flurry of articles on V.Ships this week had tongues wagging. Close Brothers had made a fortune. Management would be rich. Shipmanagement is the place to be.

In fact as any shipmanager will tell you, it is a good business, but a hard business, and a demanding business. It’s also an important one, maybe never more so. Its also competitive, a service and a people business – and a private one.

Thus no wonder there was more mis-information than fact filling pages of trade publications.

In fact the process of selling Close Brothers’ 50% stake in V.Ships continues in an orderly and professional way with first round indications of interest and price still taking place. Rothschild is leading the process for Close Brothers. Interested parties include both financial and strategic parties.

The process will follow the normal path, first round parties will be qualified, management will present and a second round will take place with a decision maybe by spring. Continue Reading

The Week in Review – 01/11/2007

Signs of the Times: Certainly Uncertain

There is no doubt that 2004-2006 were years of growth for shipping companies. Not just earnings growth of course; 2006 saw earnings fall for many companies. One area of real growth was in opportunity through the expansion of shipping’s relationship with the capital markets. We see a lot of nervous energy in the early days of 2007, with various sectors trending in different directions. A warm winter in North America and Europe and full reserves in China have made December and January’s tanker market as disappointing as the summer’s tanker market was exciting…so much for seasonal trading. But not all sectors are feeling the pinch, and many players are just now able to take advantage of the opportunities that were available primarily to mainstream tanker and dry bulk players in 2004 and 2005.

Lessor First Ship Lease, for example, expands its portfolio while shipmanager V.Ships explores strategic opportunities for its owners. Hedge fund QVT debates the value in Top Tankers while Kelso nearly completes divesting its interest in Eagle Bulk and investors in Precious Shipping gauge the political situation in Thailand. Euroseas prepares for a growth spurt even as some of its contemporaries begin to reorganize. König and HSH create a product to draw new investors into shipping while tanker analysts debate supply and demand dynamics. And of course the debt market marches on. Continue Reading

The Official Guide To Marine Finance Providers

Shipping Index