Links

The Week in Review – 02/01/2007

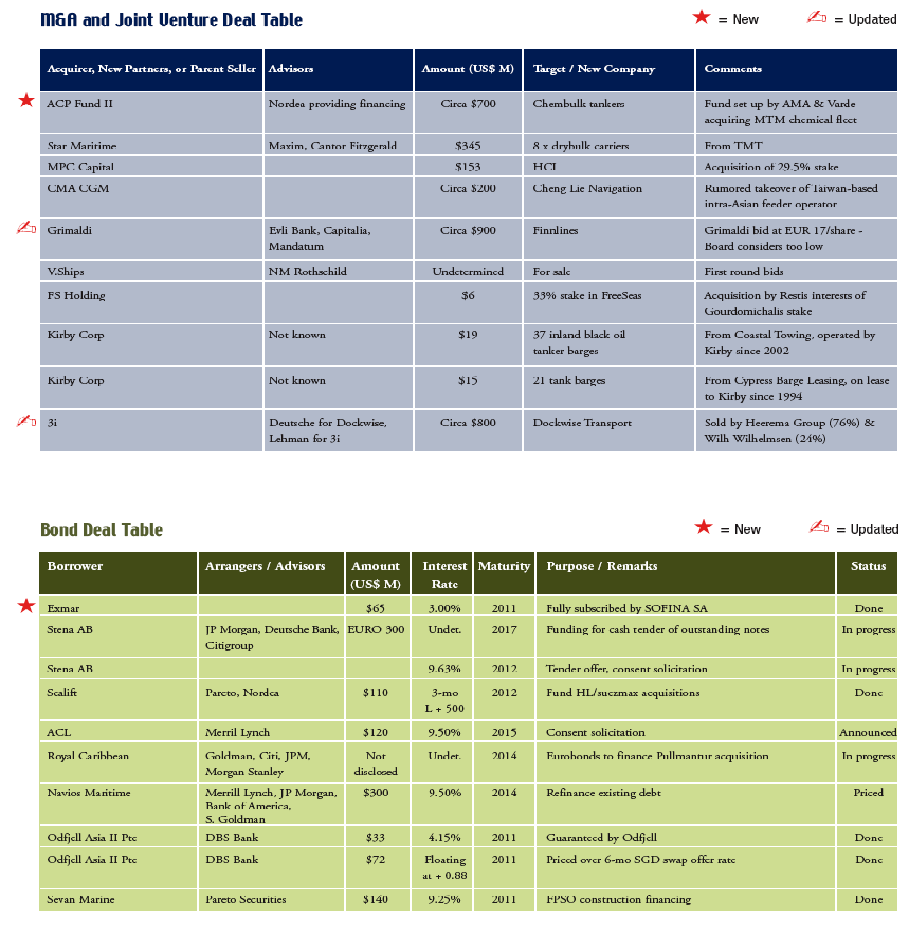

Chembulk Tanker Fleet Acquired by Private Equity

AMA Capital Partners in conjunction with their private equity partners Varde, through ACP Fund II have acquired the specialty tanker assets of Doug McShane and Christina Tan’s Chembulk in a deal that market rumors based on current comparable vessel prices peg at around $700 million. Nordea will provide financing for the deal, and reportedly were most helpful as the very private deal progressed. The tankers operate under the trade name Chembulk Trading.

McShane and Tan, husband and wife, built the impressive fleet over the past 10 years. Offices are located in Singapore, Hong Kong, the Netherlands and Westport, Connecticut. The company enjoys a sterling reputation. McShane and Tan will retain their chartered-in drybulk fleet and operations, Strategic Bulk Carriers.

AMA Capital Partners are not new at owning big-ticket assets. Last year they successfully acquired the remaining PLM Funds through ACP Fund I, and systematically monetized that portfolio of ships: 2 MR tankers and 2 Gearless Bulkers, 100,000 TEU of containers and 12 aircraft within a Fund mandated time frame. ACP I also acquired 4x 3,500 teu ships on bareboat to Zim through two K/Ss. Continue Reading

M&A: Financial Buyers, Niche Players & Two Special Deals

This year’s M&A market was smaller in volume than that of 2005, but also more interesting. With a total volume of around $11.3 billion, the 2006 M&A market falls short of 2005′s $14.4 billion in volume, yet the smaller numbers belie the fact that there are more than 20% more deals in 2006.

The difference can be attributed to a few large transactions in 2005, and also depends on how you cut the numbers. Take away TUI’s $2.3 billion acquisition of CP Ships and AP Moller’s $2.7 billion acquisition of Royal P&O Nedlloyd, both in 2005, and the numbers tell a different story. The story has to do both with a shift in sectors and a growth in consolidating activity among smaller companies. While the name of the game in 2005 was liner consolidation, the big-ticket transactions we witnessed in 2006 tended to be within the rig and infrastructure industries. While many of these deals involve some of the same players as pure shipping deals and are followed in these pages, it does not seem appropriate to count them in shipping M&A volume. The sale of shipping services companies such as Heidenreich Marine, however, are counted based on the idea that the commercial, operational and other services provided by such companies overlap with those some shipping companies provide for themselves and thus their value should be considered a part of the shipping sector.

That said, on the one hand what we saw in 2006 was a proliferation of niche sector M&A deals. A common market perception that vessel values had peaked put pressure on valuations and made many large-scale acquisitions appear less attractive than they would have as vessel values were still rising. The search for value therefore became more focused on sectors like the Jones Act or chemical tanker sectors where regulations or general market conditions protected acquirers from the threat of over supply in the medium term. Continue Reading

Out-of the-Box Thinking or the Structured Finance Award

One transaction executed this year was sufficiently impressive and out of the ordinary to cause the Marine Money editors to see the need to create a new category of award as we view it as a precursor of the future. No matter what our more jaded readership may think, it is not a quick solution just to reward another institution as a consequence of a plethora of good deals. We do not take additions lightly. The transaction is, as you will see below, a public debt deal; yet it is also so much more than that. It represents the recurrent themes of out of the box thinking, best practices and imagination gone wild on the balance sheet.

As a consequence of large capital requirements, credit capacity constraints and a desire to shift risk, owners saw the limitations of the available standard finance products to deal with these issues and sat down with their bankers to see if any of the existing structured finance tools could be applied to shipping. Although banks had previously securitized their loan portfolios, it was BNP Paribas that put together the first securitization of a fleet of vessels rated by Standard & Poor’s and Moody’s. It was their experience in and lessons learned from aircraft financing that were clearly critical to making this happen. Continue Reading

Restructuring Deals – Breathing Life into Worthy Projects

In a year of relative prosperity there were as might be expected few restructurings. What to do with an Award that a few years ago dominated these pages? The race came down to two very different deals both in terms of size and sector, and while we may be accused of flipping a coin, there is no proof of that!

We have observed first hand restructurings and understand how difficult it can be to coordinate interests and resolve problems in a fashion that does not simply temporarily bandage a wound but enables future health and value creation. Relationships, strong understanding of the business and thoughtful structuring are common hallmarks, but easier said than done.

So we start by congratulating both deals and all the parties involved. Continue Reading

“Junk” – The Public Debt Award

It was another interesting year in the public debt market. The bond market continued to be active with transactions that ran the gamut from the simplicity of straight issuance to the complexity of project financing. In the latter category, US Shipping (“USS”), for example, accessed the bond market to assist in the capitalization of its joint venture with The Blackstone Group and Lehman Brothers, which will warehouse USS’s fleet renewal program. Also of interest, was the final resolution of the Navigator Gas saga with the bondholders finally getting control of the company and its vessels.

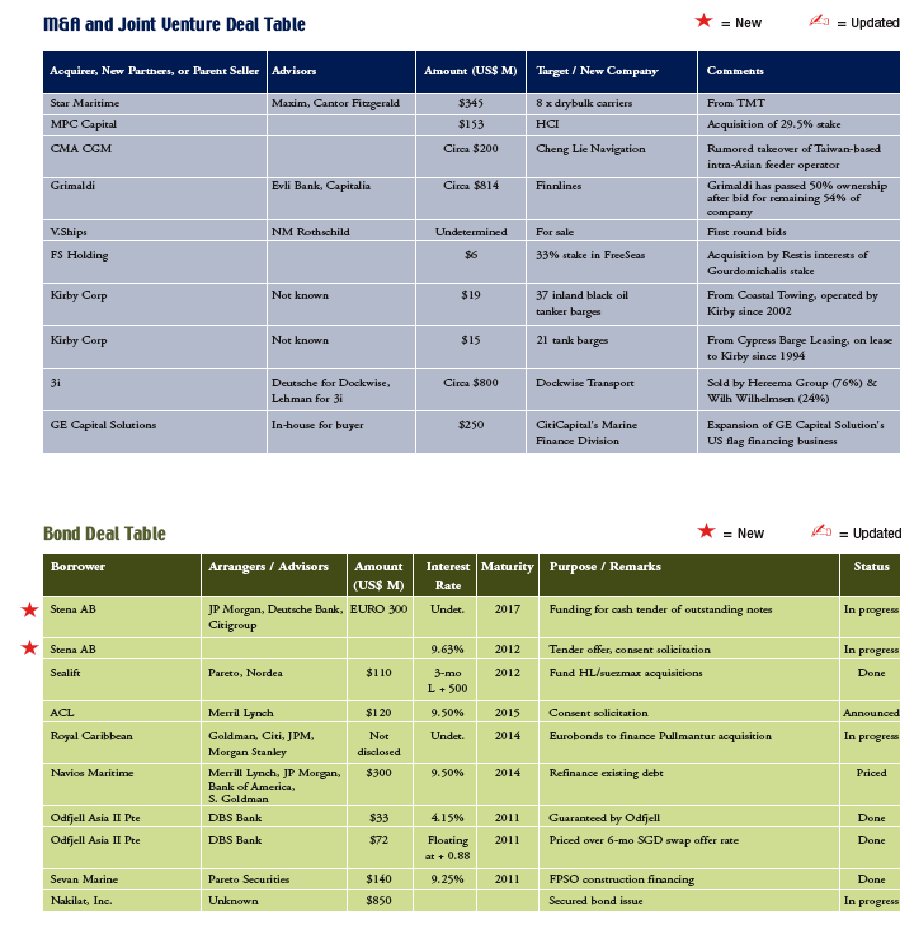

Of the various transactions that occurred this year, two transactions and a trend stood out. High yield bonds returned in the US, a niche player successfully issued in Europe, and a new capital of high yield evolved. With the assistance of Merrill Lynch and JP Morgan, Angeliki Frangou’s Navios Maritime issued high yield bonds for the first time since the junk bond debacle of the late 1990s. Navios does not fear leverage and manages it well. So it was no surprise that in December, the company announced the successful sale of its $300 million of 9.5% Senior Notes due 2014, the proceeds of which were used to refinance its existing credit facility with HSH Nordbank. Priced at 99.316% to yield 9.625%, the Notes were offered in the United States only to qualified institutional buyers pursuant to Rule 144A. The Notes will initially be guaranteed by all of Navios’ existing subsidiaries, other than its South American business. One of the key attractions of the refinancing was the lack of principal amortization during the tenor, which is typical of these deals. Investors were attracted by the company’s charter coverage, the value of its purchase options, the company’s low break-even levels, and the dynamics of the dry bulk market in the intermediate term. For many US investors this was a first time experience with dry bulk shipping company bonds. As to the company, the relatively low EBITDA multiple at which its shares trade made bonds a dramatically less expensive way to raise growth funding than the issuance of additional equity. Continue Reading

Bank Debt in 2006: Public Companies Take on Dry Powder & Lenders Wander the World

If the international ship finance business is a body, comprising complex system of vital organs, then commercial bank debt is its heart – and as you can see from looking just about every single transaction highlighted in this special issue of Marine Money – nothing functions without it.

Whether you are talking about XL Capital’s $1 billion investment grade credit wrap for CMA-CGM, Top Tankers sale/leaseback in Korea, Odfjell bonds in Norway, Quintana’s acquisition of Metrobulk or the dozens and dozens of public and private equity deals living and breathing in New York these days, the reality is that the financial returns needed to create virtually every capital structure in the global shipping industry are nourished by leverage – and that leverage comes from the bank debt market.

And so long as transaction activity is increasing in size and complexity, as it has been for years, we think that the market for bank debt will become even more vibrant.

Not surprisingly, the year 2006 was another great one for the business of commercial ship lending. According to Dealogic, syndicated loan volume was up from $60 billion in 2005 to $70 billion in 2006. This increase was thanks to high asset prices, which can be seen in figure 1. Another reason, we think, for the increased deal volume is simply that there are more public companies than ever before and these companies are legally bound to file details of their financing with Securities and Exchange Commission, which means they get included in the figures compiled by data processors like Dealogic. Continue Reading

So Much to Choose

With apologies to all Trekkies: “Awards the final frontier. These are the voyages of the Starship Marine Money. Its continuing mission: to explore strange new deals, to seek out the winning capital providers, to go boldly where no sane person has gone before.”

With apologies to all Trekkies: “Awards the final frontier. These are the voyages of the Starship Marine Money. Its continuing mission: to explore strange new deals, to seek out the winning capital providers, to go boldly where no sane person has gone before.”

It is a wonderful task to celebrate the accomplishments of so many and an industry so creative that each year brings yet another crop of deals, projects and transactions that stretch our views of how business is best transacted. The Marine Money team follows the daily volume of the activity with a keen interest. We admire the tried and true, appreciate the real meaning of relationships, marvel at the cycles – not just shipping’s but recently and more obviously in finance – and respect the enormous amount of good new thinking and structures. We also see a wealth of options for shipowners in financial markets around the world, perhaps driven by government stimuli or more dramatically from fundamental shifts in the flow of funds.

There are three absolute truths about this issue. One, it is true what they say about us, at least sometimes – that we never saw a deal we did not like. The simple fact is we appreciate the creativity, thought, risk and hard work involved in concluding a transaction. That doesn’t mean we would put our money in every deal, but we do admire the men, women and businesses that try to build things. This issue is a celebration and we make no bones about recognizing achievement with Awards. Continue Reading

Frontline Exercises Purchase Option with Dr. Peters, Makes a Buck or Two

Frontline Exercises Purchase Option with Dr. Peters, Makes a Buck or Two

Frontline Exercises Purchase Option with Dr. Peters, Makes a Buck or Two

The Official Guide To Marine Finance Providers

Shipping Index