Links

Equity – 03/22/2007

Marinakis Returns

Despite concerns that the multitude of shipping IPOs in 2004 and 2005 would ultimately turn investors away from shipping just as the high yield bond issues of the late 90s did, almost the opposite has happened. In March of 2007, there are more public shipping companies than ever before, with new ones coming to market faster than old ones can be bought up or consolidated. The IPO frenzy of 2004 ultimately, though not gracefully, educated a world if investors about shipping and world of shipowners about public investors. Investment bankers faced over and over with the fundamentals of the various shipping sectors meanwhile began to dream up more creative ways of packaging the industry attractively for investors.

If there is anyone who epitomizes this process, it is Evangelos Marinakis of Capital Maritime. With a history as a successful shipowner in the Greek tradition, Mr. Marinakis first attempted to sell his company to investors in New York in the spring and summer of 2005. He and his team probably saw their company as very saleable – with experienced management, a strong track record, diversified assets, a competent in-house management team, and investment in newbuildings for future growth in the promising product tanker sector. Not surprisingly, they were somewhat disappointed with the lukewarm reception they received from investors. Confident that his company was worth more than the price these investors were willing to pay, Mr. Marinakis withdrew his initial deal and stepped back from the frenzied New York capital markets. Continue Reading

Equity – 03/15/2007

Two More Greek Sponsored IPOs To Build on MLP Universe

In a development suggesting that demand for Master Limited Partnership-type structures is actually creating a supply of such deals, two new Greek sponsored shipping IPOs are making their way toward Wall Street – and should make landfall just in time for Marine Money Week in June!

This is hardly surprising. One of the amazing things about the shipping industry is that by tweaking debt levels and amortization structures, charter terms and tenors and vessel age, shipowners and investment banks can tailor deals to meet investor demand. Put another way, shipowners have the ingredients to cook-up just about any quantity of just about any product that investors have an appetite to eat, from SPACs to MLPs, “China Plays” to “Midstream Energy Transportation.” Continue Reading

Market Commentary – 03/15/2007

Extraordinary or Ordinary?

It’s earnings season once again and along with announcements of earnings, companies are declaring the latest quarterly dividends. It is easy to get lulled into a false sense of security as dividends continue and companies report percentage days contracted for the current as well as future years. The latter, of course, shows earnings visibility, steady cash flow and downside protection in difficult markets. In a nutshell, shareholders are thinking, “what me worry.”

Based on recent events, a couple of owners, on the other hand, may be asking why do bad things happen to good people? First, Navios reported strong 4th quarter and year-end results that however were impacted by a one-time charge of $5.4 million relating to a writeoff of a doubtful receivable. The company described this as a counter party problem in its investor conference call. It appears that Navios may have been a victim, like many others, of the default by Canada’s North American Steamship Line (“NASL”) under its FFA agreements in November. Apparently, NASL was shorting the market in anticipation of a rate decline that never came and unfortunately these were not hedges but were speculative bets. And with no gains on the physical side, substantial losses were incurred. Continue Reading

Research Notes – 03/15/2007

Golden Ocean CEO Herman Billung presented a very optimistic picture of the dry bulk market to analysts at Pareto today, pointing out that massive dry bulk demand in the second half of 2006 had continued into 2007, while record port congestion has further bolstered rates. Secondhand values for bulk carriers continue to increase significantly and have reached all time high levels, indicating a belief in the market among dry bulk vessel buyers and owners.

Pareto analysts share a bullish view on the dry bulk sector, but express more concern over the market for crude oil transport. Though they note that the crude tanker market has improved, they are concerned about high US crude inventories, seasonally lower demand and a busy VLCC delivery schedule, the majority of which has yet to occur. They are confident in a strong market for clean product and chemical tankers, noting that solid rates are not yet reflected in the corresponding share prices, with valuations as illustrated in the graph that accompanies this article. Continue Reading

Company News – 03/15/2007

FR8 to NAVIG8

FR8 was established in 2003 as a joint venture with Projector Ltd, a prominent oil trader, who provided a core volume of cargos and access to attractive time charter opportunities. FR8 is not your father’s shipping company. With its owned fleet, time chartered fleet and management companies, it resembles a normal shipping company except for the fact that its brain is wired and its perspective is that of a trader. In short, this is the world of seeking arbitrage opportunities, while managing risk and not just looking at “last done.”

The company controls a fleet of approximately 30 product tankers via a combination of time charters, joint ventures, ownership and commercial agreements. Of the controlled fleet, the company together with its joint venture partners own two LR product tankers and eleven MR tankers (including the orderbook) and have purchase options on three more vessels. Continue Reading

People & Places – 03/08/2007

Marine Money Asia Gets Ready for the Year of the Golden Pig

As Marine Money Asia has celebrated its one-year anniversary in Singapore we are pleased to announce the addition of Mr. Rodricks Wong as our new Financial Analyst. Mr. Wong is a graduate of Singapore Management University and had 16 months of project development experience with Singapore based Kontiki Enterprises Ltd before he started with us. Mr. Wong’s responsibility will be to cover the Asian ship finance industry and produce bi-monthly reports on the activity thru the issuance of our special online newsletter Marine Money – Asia Edition. To see the latest issue and subscribe to this product visit the following link http://www.marinemoney.com/MMAsia/MMA060307.pdf

We are still looking for a Sales Manager to be based in our Singapore office and welcome any applications by email; pbogen@marinemoney.com -If, you have any sons or daughters who would like to kick-start a career in ship finance, we can offer this opportunity today! Continue Reading

Spotlight on Oceanaut – 03/08/2007

Hiring a Personal Shopper

We commented a couple weeks ago on the initial public offering of Oceanaut, a blank check company sponsored by Excel Maritime and its key employees. With the deal successfully completed with a total capital raise of $161 million on Tuesday, we thought it might be worth taking a closer look at the transaction.

But perhaps before we do, we should explain the title of this piece. In our mind, if an investor is interested in investing in the shipping space, he has innumerable potential investment opportunities in the public arena that would suit any requirement. Whether the investor is looking at a particular sector, growth versus yield or a niche player etc., all are available as publicly traded entities with visible earnings streams and known assets. Furthermore, the analyst community has broken down the numbers in a multitude of ways and rated each of them accordingly. So why would anyone invest in a black check company with the hope that in 18 months the company will find an investment opportunity? The only thing we can think of is that the investing community believes the promoters involved can find an off-market special deal, in effect a golden nugget. As part of a new company the deal would not be impacted by the excess baggage an existing company carries around and, in that sense, the deal is more a pure play. Rather than sift through the many public stocks, the SPAC investor instead hires a “personal shopper” to find the perfect “gift.” Or perhaps, in its most simple sense, it is just the thrill of the deal. Continue Reading

The Week in Review – 03/08/2007

Some Beautiful Returns!

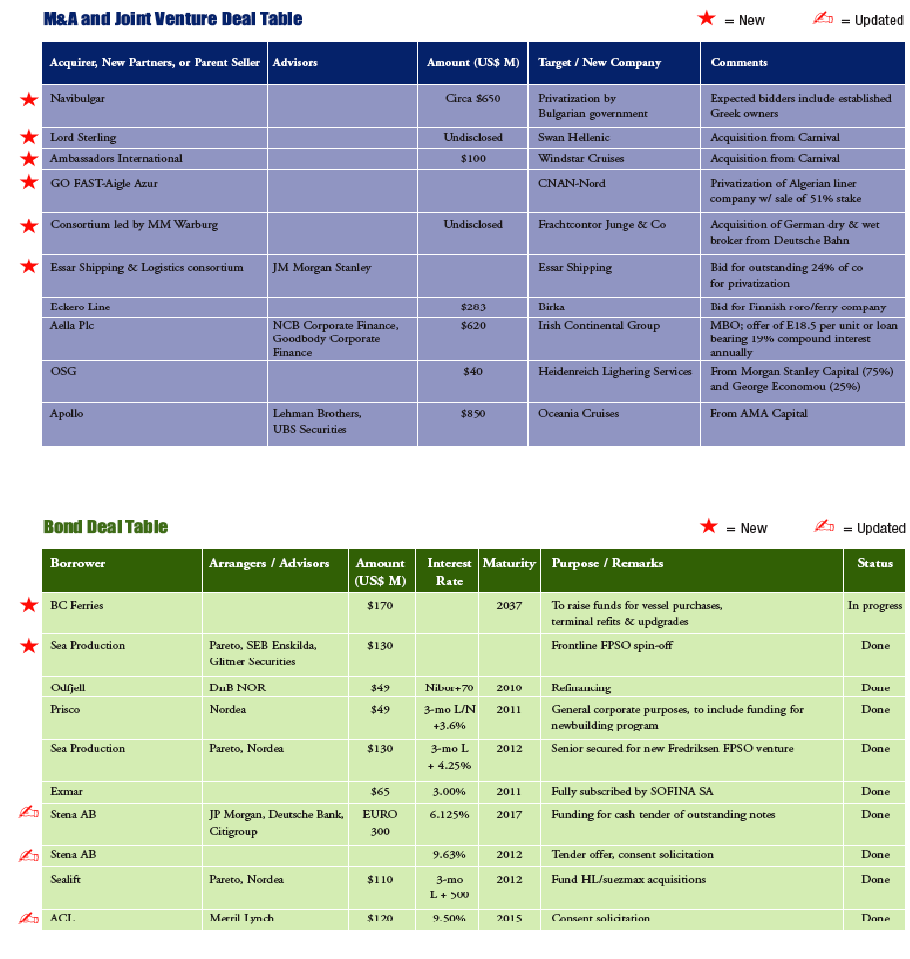

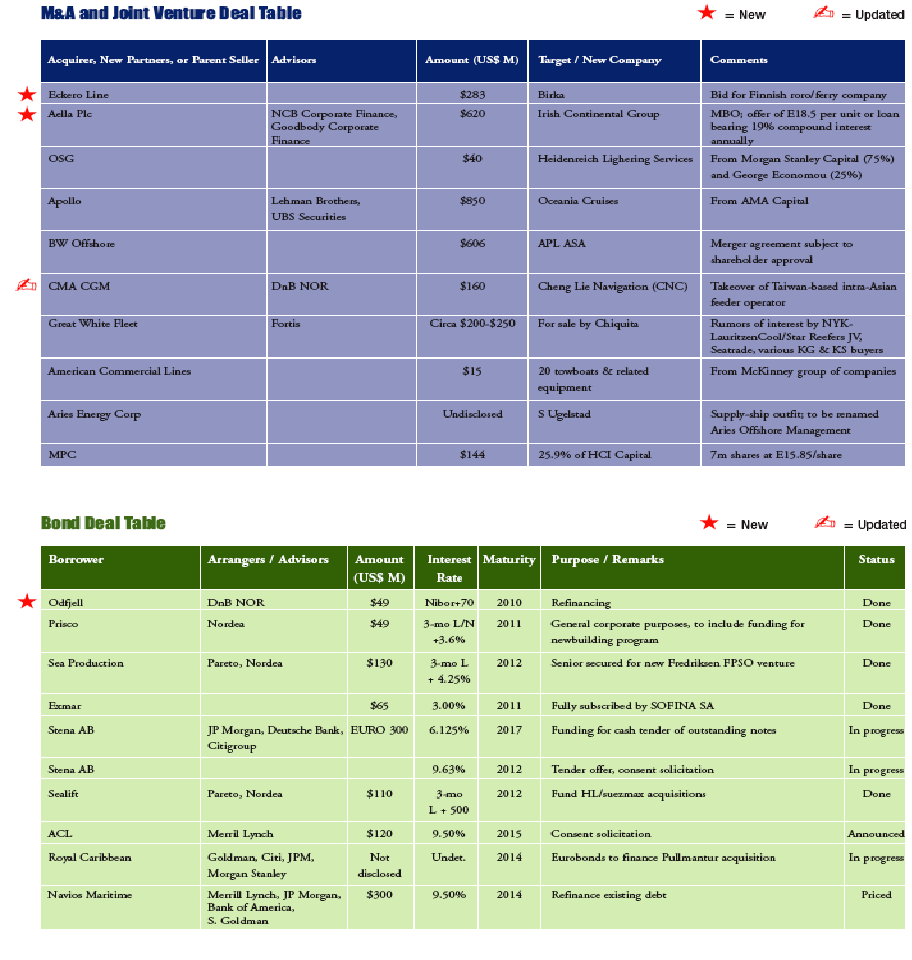

Last week’s news on the strategic investment made by Apollo Management into the Frank Del Rio led Oceania Cruises was notable for the$850 million amount the 5- year-old cruise line commanded. What deserves a bit more attention is the return that equates to. Our readers will recall that shortly after 9/11 Oceania’s current cruise-ships were effectively valueless. A consortium of banks, led boldly by Calyon, rather than panic and sell the vessels for a mere $90 million, then the best offer, formed Cruiseinvest to own the ships. A plan to recover value developed with Frank, AMA and themselves was worked out. Frank raised $14 million dollars for what was effectively a start up marketing company, which then chartered in the three vessels. It was a risky bet for sure.

But now a little math, Apollo’s $850 million assumed $375 million in debt, raised a short while ago to pay off the banks. So $850 million minus $375 million imputes an equity value of $475 million. Not too shabby a return on $14 million!

With the new funding support the company is in Europe looking at yards in Italy, Germany, France and Finland for new buildings. Continue Reading

The Official Guide To Marine Finance Providers

Shipping Index