Links

The Week in Review – 06/28/2007

Early Independence Day

Last Friday, a mere two weeks since its last sale, OSG announced that it sold 3,001,500 shares or the last of the shares it owned in Double Hull Tankers in its third secondary offering. The sale of was made pursuant to DHT’s existing shelf registration and was underwritten by Merrill Lynch. OSG expects to book a gain of $9 million in the second quarter. Free of its parent OSG and with Tom Kjeldsberg as its new business development officer, it will be interesting to see how the company evolves. Let the games begin!

Strange Bedfellows

Top Tankers announced today that it had placed 2.1 million shares with a strategic investor. The shares were placed with companies affiliated with George Economou and raised proceeds of $14.3 million which the company will use for acquisitions, working capital and general corporate purposes. The shares were issued under Top’s effective shelf registration statement in connection with the company’s controlled equity offering program.

With this purchase, Mr. Economou controls 3.7 million shares representing 10.72% of the company’s outstanding shares. As a symbol of his mysterious intentions, the shares were purchased through appropriately named investment vehicle Sphinx Investment Corp. Mr. Economou began purchasing shares on April 27 at $4.0753 per share with the last purchase on June 26 at $6.88 per share. The average price he paid per share is $6.264.

The second largest owner of shares is QVT Financial GP LLC, which currently controls 1,591,326 shares representing 4.91% of the shares outstanding.

As for Economou and Pistiolis working together, this is not the only example that has come about as late. The two are also understood to have invested in a venture called Ocean Hotels, Mr. Economou to the tune of $20 million and Mr. Pistiolis to the tune of $8 million.

For the moment the couple is enjoying the honeymoon. Mr. Pistiolis, President and CEO of Top Tankers, stated, ” This strategic investment constitutes a vote of confidence in our company and its management. We welcome Mr. Economou’s valued participation.” Management will certainly be challenged, as we know Mr. Economou is not a passive investor.

Stymied

Surely, it is getting harder to report the news these days. In trying to report on BW Group’s recent $500 million bond offering we hit the proverbial wall. Distribution of the prospectus was restricted to certain types of investors, which obviously precluded us. We did however manage to eek out the following information. The underwriters were Morgan Stanley and HSBC. With the final pricing at the tight end of the range, the offering, which targeted institutions, attracted an orderbook of approximately $1.6 billion and thus was more than 3x oversubscribed.

The Little Engine that Could

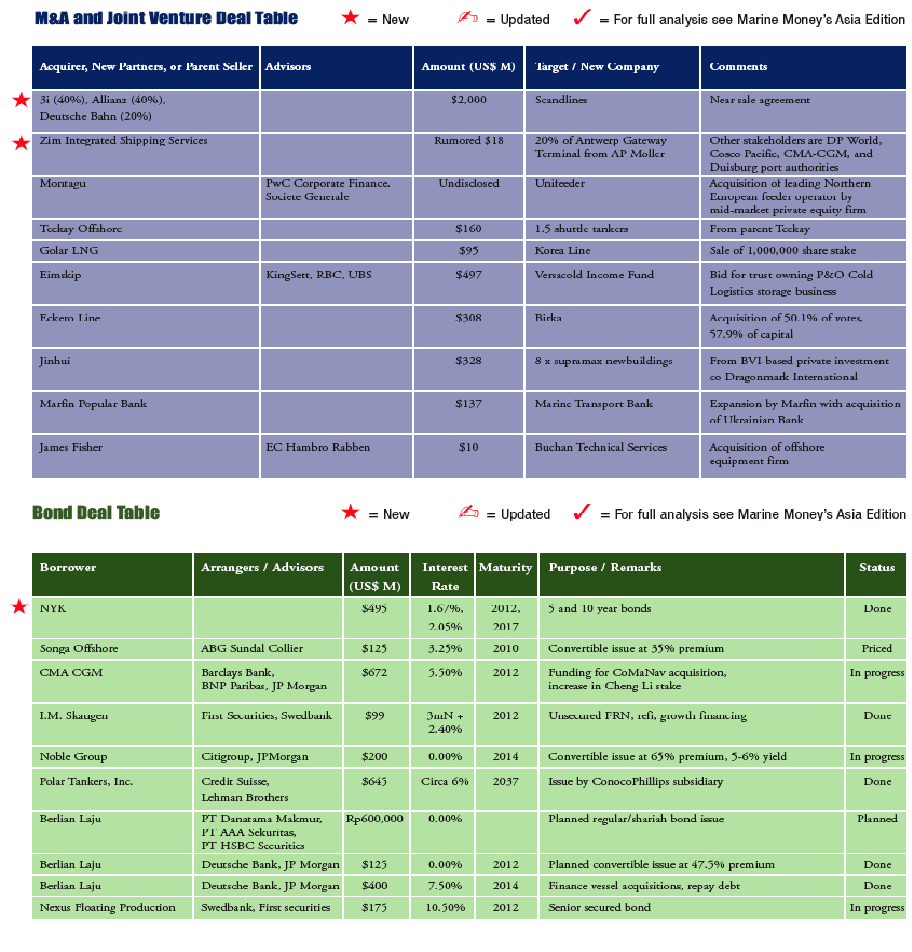

Our sister magazine, Marine Money Asia, has provided detailed coverage of PT Berlian Laju Tanker Tbk’s (“BLT”) recent serial issuances of debt.We became intrigued by the activity and decided to take a closer look at what they were doing so that we might provide some insights to our broader readership.

By way of background, BLT was established in Indonesia in 1981 and purchased its first two oil tankers in 1982. In 1986, the company entered into the chemical transportation business and in 1989 into the gas transportation business. In 1990, the company completed its initial public offering and became the first Indonesian company listed both on the Jakarta and Surabaya stock exchanges. Since then the company has grown and currently owns and controls a fleet of 62 vessels. And finally in 2006, the company completed the listing of its shares on the SGX-ST in Singapore meaning its shares are currently listed on three different exchanges.

In April 2007, the company entered into a broad financing plan to largely refinance debt as well as to borrow for general corporate purposes including vessel acquisitions. As part of this plan and to facilitate the financing transactions, the company established BLT Finance B.V. in the Netherlands as a limited liability company, which is a wholly owned subsidiary of BLT. A Dutch company was chosen for both commercial as well as tax reasons.

The notes and bonds issued by BLT Finance are senior in ranking but unsecured. BLT, however, fully guarantees the obligations of the finance subsidiary. A cautionary note regarding the guarantee is in order. Although BLT has waived its rights under Indonesian law to require an obligee to exhaust its legal remedies against the obligor’s assets on a guaranteed obligation prior to the obligee exercising its right under the related guarantee, there is no assurance that Indonesian courts will not impose an obligation to pursue all legal remedies against the issuer first, as a consequence of the uncertainty surrounding the outcome of specific legal cases there. In short, the prospectus reminds investors that they will be exposed to a legal system subject to considerable discretion and uncertainty. These issues may date back to the Pertamina experience in the mid-70s.

The plan involved three offerings: Notes, Bonds and Rupiah Bonds. In May, BLT Finance took the first step successfully issuing $400 million of 7.5% Guaranteed Senior Notes due 2014. It was however the second step that truly intrigued us. Last week, BLT Finance issued $125 million of Zero Coupon Guaranteed Convertible Bonds due 2012 (the “Bonds”).

This is not the first time BLT has been able to win such favorable pricing. In fact, BLT had issued $50 million in convertible bonds in December 2005, which was the first such convertible offering by any publicly listed Indonesian company. In fact it was so successful that it was converted within 6 months of launch, which was largely attributable to a 100% increase in BLT’s share price during that period.

In fact, this bond was the third convertible offering in Indonesia and like its predecessor also appears poised for success, as it was oversubscribed 5x within hours of being launched. The company also was sensitive to pricing and hoping to achieve comparable success with its prior offering did not go after the tightest pricing possible.

In effect, if it were a simple zero, the company would repay the bondholders 129.58% at maturity in 2012. Interest expense would be accrued on the income statement although no cash would exchange hands until maturity. But that is where it gets interesting. The bonds are convertible into ordinary BLT shares at a conversion price of SGD 0.4965 per share initially, a premium of 45%. Currently, the shares are trading at SGD 0.335 to 0.34. The conversion period is from June 27, 2007 through April 17, 2012. Importantly, the company has structured the transaction to avoid dilution to current shareholders by using treasury shares for the underlying shares. The treasury shares were acquired through a share buy-back program from the market. Through this structure, it is reasonably likely that the company will not have to pay cash interest and shareholders will not suffer dilution. Talk about a win-win.

BLT has the put option to redeem all of the bonds any time after two years at a price that will equate to a 5.25% gross yield. Bondholders also have the call option to redeem the bonds after three years at a price of 116.82%. There are other options covering various event risks including but not limited to tax, change of control and de-listing.

In addition, there are two other features that benefit the bondholder. The first is a cash settlement option, which allows the issuer to pay the bondholder directly in cash when they convert. The other is a result of the multiple listings of the shares. As a consequence of the multiple listings, the bondholder can look for arbitrage opportunities and sell his shares on the more liquid or profitable exchange.

It is no surprise that the issue was oversubscribed. The bondholder has a floor of a 5.25% return with unlimited upside and the company’s prospects look good. Although the bonds are not rated the earlier issued notes were rated as BB- by both S&P and Fitch. As of December 31, 2006, the balance sheet is reasonably strong with positive working capital including $146 million in cash and cash equivalents. In terms of leverage, the net debt to capitalization is a conservative 32.7% and as a large part of this exercise was to refinance expensive debt it is likely the leverage will remain at or near these levels. Historic revenues and earnings over the three-year period have shown substantial growth. And now there is cash for accretive acquisitions, which will further bolster earnings.

The third leg of the financing plan was also a great success. BLT expanded its Rupiah denominated bonds by 50% to IDR 900 billion. Even with the increase the deal was oversubscribed with investors applying for IDR 1.5 trillion. Of the total, IDR 200 billion were Shariah bonds with the balance conventional paper.

Watch closely as this “little engine” becomes an increasingly major player.

Thommessen Banking & Finance Unit Gets New Partner

People seem to change jobs like it’s their job in the ship finance industry, so we were happy to hear that leading Norwegian business law firm Thommessen has promoted Siri Wennevik to Partner. Ms. Wennevik has also worked at Andersen Legal and Vogt & Wiig, starting at Thommessen as senior associate in 2004. Her core expertise is within the finance market, with special focus on the shipping and offshore sectors.

NASDAQ Closing – 06/21/2007

Marine Money Chairman Jim Lawrence led a group of guests to the NASDAQ market headquarters in Times Square to ring the closing bell. Charlotte Crosswell, head of NASDAQ International introduced Jim and noted that Marine Money Week is synonymous with making and closing deals. Most recently, Capital Product Partners, Euroseas and Oceanfreight have listed on the NASDAQ, adding to the total of 11 shipping companies listed today on the exchange. Jim Lawrence continued to celebrate the success of shipping companies on the public markets, rewarding their shareholders with an overall 23% return! Mr. Lawrence was then honored with a commemorative crystal and led the ringing of the closing bell. Continue Reading

And the Winner is………!

As the black box generated the results, we here at Marine Money breathed a sigh of relief balanced with a tinge of regret. We did not have to create a new category of best shipping company based outside of South Africa as we feared might be necessary. After a string of two consecutive wins, Grindrod did not repeat, but came awfully close, finishing in the number six spot overall after another excellent performance.

But that is history. This year’s winner of Marine Money’s 17th Annual Rankings Awards is American Commercial Lines Inc. (“ACL”), which also happens to be one of five members from last year’s freshman class to occupy spots in this year’s top ten. This was quite an accomplishment as our universe of ranked stocks grew to 86 this year. Continue Reading

People & Places – 06/14/2007

HSH Goes Greek

HSH Nordbank has announced plans to open a representative offering in Greece. With a shipping loan portfolio of $40.9 billion at the beginning of 2007, HSH according to our records has more capital committed to shipping than any other bank on earth. Although only about 10% of these commitments are in the Greek market, that number represents $4.2 billion in loans so we don’t imagine their office will be under-utilized – and of course there is plenty of room for more growth!

Anke Struebing to Leave Nord LB, Join Deutsche Schiffsbank

After seven years at Nord LB, Anke Struebing has announced plans to move on to look for new challenges with a position at Deutsche Schiffsbank in Bremen. Yvonne Ahlendorf and Claudia Herrmann will be taking on Anke’s responsibilities at Nord LB. Congratulations and best of luck to all! Continue Reading

Company Spotlight – 06/14/2007

Of Ships, Planes and Leasing Companies

On Tuesday, approximately 22 months since its IPO, Seaspan, with the assistance of The IGB Group, held it first Analyst/Investor Luncheon at New York’s Palace Hotel. The event was well attended and the company took the opportunity to take a look back at its accomplishments, discuss its goals, strategies and strengths, and then answer investors’ questions, all in what Gerry Wang aptly described as West Coast casual.

The first thing we observed was that the company had somehow managed to have its entire senior management team here in one place despite the multitudinous deals that are in process, running 27 ships and supervising the construction on another 28 of which 15 will be constructed in China. It appeared that Peter Curtis, Vice President of Seaspan Ship Management, traveled the furthest arriving directly from a tour of the Chinese shipyards where he was inspecting the progress of the newbuildings there. Continue Reading

The Week in Review – 06/14/2007

Exploring New Paths to Public Equity

There’s more than one way to skin a cat, as they say. And never before has this been more true for a shipowner looking to raise outside equity than today. As the global capital markets continue to grow to ever new heights of complexity and depths of liquidity, it’s becoming ever more clear that the traditional thresholds and standards needed to access the public equity markets can be flexible if you take the right approach.

The recent Globus Maritime IPO and in-progress Paragon Shipping listing bring this phenomenon into relief. For those not familiar with these deals, Globus this month became the second shipping company to list on the London AIM (Alternative Investment Market). Paragon Shipping had actually considered listing on the AIM itself before turning to a Rule 144A private placement in the US. This month Paragon made its first public filings in preparation for the listing of its shares and warrants on the Nasdaq over-the-counter market in the US. Continue Reading

The Week in Review – 06/07/2007

It’s been quite a week for selling shares. OSG filed to sell its entire stake in spin-off Double Hull Tankers, selling a substantial portion of that stake through Merrill Lynch and UBS nearly immediately after its registration became effective. Meanwhile Fredriksen’s public LNG and tanker companies were both busy selling off shareholdings, with Golar LNG selling the remainder of its stake in Korea Line for $95 million and Frontline selling its entire stake in Sea Production for $67 million. At the same time the holders in Bodouroglou dry bulk venture Paragon Shipping have filed to sell off their holdings.Whether it’s a flurry ahead of a summer lull, premonitions that the market has peaked, or pure coincidence it is too early to tell. Continue Reading

Rankings Ruminations – Bye Bye OMI and other Bon Mots From over the Years

By James R. Lawrence & George Weltman

The Rankings results this year offer some food for thought. We were struck by the fact that OMI in its final stand alone year-end results finished an extremely respectable 17th, while its successful suitors D/S Torm finished 2006 in 18th position and Teekay Shipping 73rd. The cynical among us here viewed this acquisition by Torm simply as a ploy to move up in the rankings with perhaps some other ancillary benefits.

As that transaction was taking shape rumor had it in the Connecticut watering holes that one of the hidden treasures at OMI was its chartering team. We expect to see both Teekay and Torm flying high next year to account for the attractive price paid for OMI.

But, at the same time we are saddened by the departure of some key characters Messrs Stevenson, Bugbee, London and Ms. Haines who because of non-compete clauses may be forced to leave the industry for a period of time ranging from one to two years. Curiously, the higher the level in the organization the shorter the restricted period agreed. The same we are sure is not true of the size of the severance package. A loss for our industry will be a gain for another should they find the need to return to work in the interim. Continue Reading

Through the Looking Glass

By George Weltman

As the black box generated the results, we here at Marine Money breathed a sigh of relief balanced with a tinge of regret. We did not have to create a new category of best shipping company based outside of South Africa as we feared might be necessary. Nor would we be accused of fixing the results, despite the entreaties of Grindrod’s greatest fan here in our office. After a string of two consecutive wins, Grindrod did not repeat, but came awfully close, finishing in the number six spot overall after another excellent performance, but more on them later.

But that is history. This year’s winner, from the class of 2005, is American Commercial Lines Inc. (“ACL”), which also happens to be one of five members from that freshman class to occupy spots in this year’s top ten. In fact, it also happened to lead the freshmen in total return to shareholders last year. Could this be the beginning of a new streak? Continue Reading

The Official Guide To Marine Finance Providers

Shipping Index